In our previous article, Thinksmart Insurance clarified what Max Funded IUL is and the 6 benefits this life insurance program offers. However, “cost” is many clients’ main topic when learning about Max Funded IUL. Therefore, today Thinksmart Insurance will provide information on how much a Max Funded IUL policy costs and the 5 steps to participate in this insurance program. Don’t miss this article!

Cost of a Max Funded IUL Policy

A Max Funded IUL policy will include three main types of costs. Participants need to pay three specific amounts:

Insurance Costs

One of the primary costs of Max Funded IUL is the insurance cost. This is the fee that participants must pay to keep the Max Funded IUL policy active and ensure death benefits for the beneficiaries.

The insurance cost of Max Funded IUL depends on age, gender, health, and the amount of coverage selected. Typically, the insurance cost for Max Funded IUL can range from $600 to $1,200 annually for each $100,000 of coverage.

Administrative and Management Fees

In addition to insurance costs, Max Funded IUL also includes administrative and management fees. These are costs for managing and maintaining the insurance policy. These fees generally include policy processing fees, account management fees, and other expenses related to managing the Max Funded IUL policy, usually ranging from $50 to $100 per year.

Transaction and Investment Fees

Another important factor to consider when participating in the Max Funded IUL program is transaction and investment fees. These are fees related to investing in stock market indices and other transactions within the Max Funded IUL policy. These fees typically range from 0.5% to 1% of the total annual investment value.

Overall Assessment of Max Funded IUL Policy Costs

Although there are many fees to pay, a well-structured Max Funded IUL policy will provide a much higher after-tax return compared to other investment vehicles, thanks to its tax advantages and protection against market volatility.

Typically, a Max Funded IUL policy can yield an average annual return of around 5 – 10% (after fees). This figure is significantly higher than traditional investments’ 3 – 4% return (e.g., bank savings).

Comparison with Other Investment Vehicles

For a broader perspective, let’s compare Max Funded IUL with some other popular investment vehicles:

- Traditional Savings Accounts: Compared to traditional savings methods like bank deposits, Max Funded IUL provides higher after-tax returns due to its participation in the stock market.

- 401(k) and IRA: Retirement accounts like 401(k) and IRA offer tax benefits but usually lack the market protection Max Funded IUL provides. Additionally, withdrawals from 401(k) and IRA are often taxed, while withdrawals from Max Funded IUL policies are tax-free.

- Stocks and Bonds: Investing in stocks and bonds can yield high returns but comes with high risk. Max Funded IUL offers market protection – NO LOSSES even when the market is down, making it an attractive option for those wanting safe asset growth.

Cost Advantages of Max Funded IUL Over the Years

When mentioning Max Funded IUL, many people mistakenly think it is a high-cost life insurance and investment program, but this is due to their focus on the cost in the first five years. In reality, these costs decrease over time as the policy’s cash value increases and insurance costs decrease.

Typically, in the first five years, the cost of a Max Funded IUL policy may be higher than other investment vehicles. However, as participants invest long-term, the Max Funded IUL policy will begin to cover its costs, averaging only around 1-2% of the policy value per year.

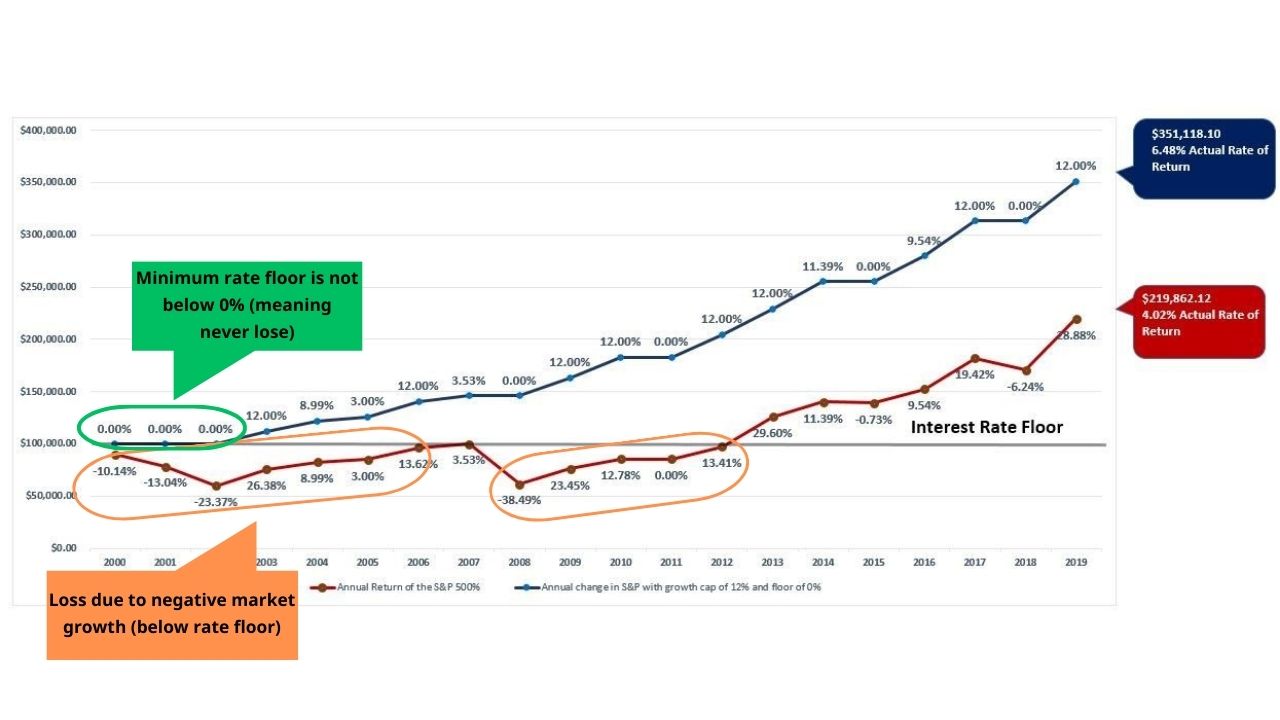

Growth of a Max Funded IUL Policy for Thinksmart Insurance Clients

The difference arises because, in the first five years, the Max Funded IUL policy uses participant contributions to cover costs such as taxes, management fees, investment fees, etc. From the sixth year, the Max Funded IUL policy uses the earnings from the previous five years to cover annual fees. Therefore, participants typically do not need to pay any additional fees.

Actual Returns from a Max Funded IUL Policy

When properly structured, Max Funded IUL policies can yield very attractive actual returns. Here are some illustrative figures:

- Average Returns: Max Funded IUL policies can provide an average annual return of 5 – 10%.

- Actual Costs: After deducting fees, the net return of a Max Funded IUL policy can reach 4 – 9%. In some years, net returns can be as high as 15%.

For example, if a Max Funded IUL policy earns a 10% return in a year, minus approximately 1% in fees, the net return is 9%. This means that only a 10% return is needed to achieve a net return of 9%. In contrast, IRA or 401(k) participants must achieve a 15% return to get a similar net return after tax.

Profits from Max Funded IUL always grow faster and safer than other Investment Programs.

Another advantage that makes Max Funded IUL policies attractive and more profitable is the Index Lock feature. Participants can monitor the market index (rate of return), and when the desired rate is achieved, they can request to lock in the rate for the entire year, ensuring a fixed interest rate regardless of market downturns. To support clients, Thinksmart Insurance monitors the market and reports the index to clients, thus helping lock in rates to optimize Max Funded IUL policy returns.

5 Steps to Participate in Max Funded IUL Policy

If you are interested in investing in Max Funded IUL, here are the basic steps to get started:

- Assess Financial Goals: First, determine your financial goals. Is Max Funded IUL suitable for your financial situation and goals? If you want to accumulate assets safely and seek tax benefits, Max Funded IUL might be a good choice.

- Find an Advisor: Max Funded IUL is a specialized investment strategy, so working with a financial expert experienced in this area is crucial. They can help you choose the right policy and develop an optimal financial strategy.

- Select a Suitable Max Funded IUL Policy: Many companies offer different Max Funded IUL policies on the market, each with different features and options. Your financial expert will help you choose the most suitable policy for your needs and financial goals.

- Design an Investment Strategy: Once you have selected a policy, the next step is to design an investment strategy. This includes maximizing insurance payments and optimizing cash value growth.

- Manage and Monitor: You need to regularly assess and adjust your strategy to ensure that your Max Funded IUL policy remains effective.

FAQs about Max Funded IUL Costs

Is Max Funded IUL expensive?

Max Funded IUL costs may be higher than other investment vehicles in the early stages, but if structured correctly, it can provide higher after-tax returns and lower costs in the long term.

Is Max Funded IUL safe?

Max Funded IUL provides a minimum return floor and protects the cash value against market volatility. Additionally, the Max Funded IUL program is backed by Allianz – a leading insurance company in the U.S. with over 130 years of experience. Therefore, Max Funded IUL is extremely safe.

When can I withdraw money from Max Funded IUL?

You can withdraw or borrow from the cash value of Max Funded IUL at any time, but note that withdrawals may affect the death benefits and cash value of the policy.

Who is Max Funded IUL suitable for?

Max Funded IUL is suitable for high-income individuals who want to safely accumulate assets and seek tax benefits, as well as those who need long-term financial protection for their families.

Conclusion

Compared to other insurance programs like Term Life or IUL Secrets, the cost of a Max Funded IUL policy is significantly higher. However, this difference only exists in the first five years of participation. After this period, Max Funded IUL participants typically do not have to pay any further fees, and the accumulated funds in the Max Funded IUL account continue to grow.

Therefore, if you are looking for a safe, effective investment solution with tax advantages, Max Funded IUL will be an excellent choice. Essentially, Max Funded IUL is still a life insurance program, so if you are unsure whether to participate, consider joining today to achieve greater investment results. Remember, the younger you are, the lower the Max Funded IUL policy costs, the higher the protection, and the greater the returns.

Thinksmart Insurance has provided information about the costs of Max Funded IUL policies. If you have any questions or are interested in this high-yield life insurance program, call our hotline at (678) 722 3447, send us a message on Messenger, or email us at Support@Thinksmartinsurance.com.

Thinksmart Insurance

Thinksmart Insurance