In the insurance and finance sectors, the Index Lock concept is becoming increasingly popular, especially during market volatility. The Index Lock feature allows investors to protect profits based on market index fluctuations without directly investing in high-risk assets.

What is the Index Lock feature?

The Index Lock feature is essentially a tool that allows investors to “lock in” the value of a financial index (such as a stock index) at the most advantageous point in time. At this point, profits will be calculated based on the locked value, protecting them from unpredictable future fluctuations, regardless of whether the index increases or decreases afterward.

The term “Index Lock” often appears in Unit-Linked Insurance Plans (ULIPs) and Fixed-indexed annuities (FIAs). This powerful tool helps insurance investors safeguard profits and mitigate risks, even in volatile markets.

How does the Index Lock feature work in insurance?

The Index Lock feature works by locking the value of a financial index (such as the S&P 500) when it reaches a certain peak, thereby protecting the accumulated profits.

Specifically, if you invest in an index-linked life insurance product when the market index reaches an optimal level, you can activate the Index Lock feature to preserve that profit level. If the market subsequently declines, your investment value remains protected at the locked level, preventing losses.

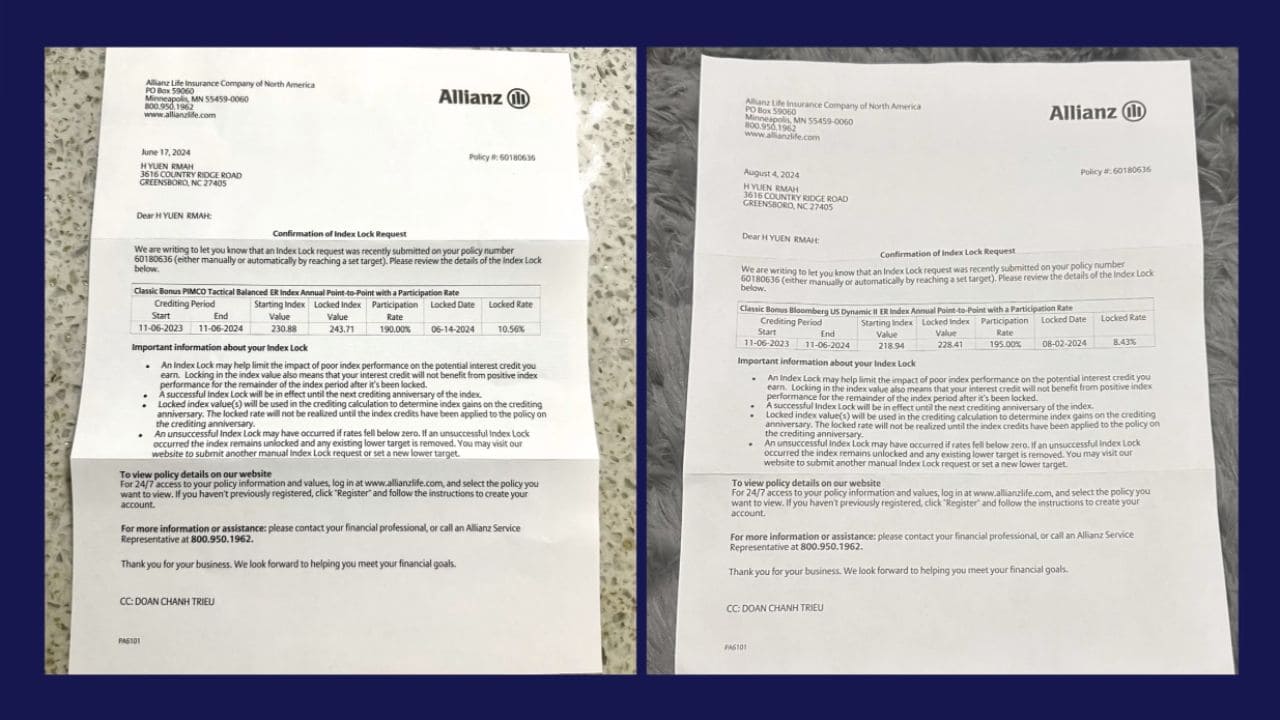

Example:

Mr. A participates in a Max Funded IUL, whose interest rate depends on the S&P 500 index. At the beginning of the year, the S&P 500 index reached 6.5%. In the mid-year, the index increased to 11.8%, and Mr. A decided to activate the Index Lock feature to secure this growth rate. By the end of the year, the S&P 500 had dropped to -3.5%, but thanks to the Index Lock feature, Mr. A still enjoys a profit at the 11.8% rate, even though the market fell into negative territory.

Some basic mechanisms of the Index Lock feature include:

- Locking the highest point value: Investors can choose to lock in the highest point value, preserving the value even if the market declines.

- Profit protection: Once the index is locked, all previously accumulated profits are safeguarded from any market downturns.

Benefits of the Index Lock feature

The Index Lock feature is not only a tool to protect profits but also one of the best ways to ensure the safety of long-term insurance investments. Below are some key benefits of the Index Lock feature:

- Profit protection in volatile markets: During financial market instability with strong fluctuations, the Index Lock feature helps you maintain the profits you’ve already achieved, without worrying about declines in investment value.

- Risk reduction: With the Index Lock feature, you don’t have to worry about losing profits due to market volatility. This is especially useful for those nearing the time they need to access their investment funds, such as retirement.

- Maximizing safe profits: The Index Lock feature helps investors protect their initial investment and maximize profit potential, particularly during periods of strong market growth.

- Flexibility: Investors have the flexibility to choose when to lock in their profits to ensure optimal gains based on market movements.

Drawbacks of the Index Lock feature

Despite its many benefits, the Index Lock feature is not without its limitations. Below are some disadvantages to consider:

- No undoing after locking: Once you’ve locked in profits, you cannot unlock them to take advantage of further profit opportunities if the market continues to rise.

Example:

Mr. C activated the Index Lock feature when the stock index reached 8.25%. However, after locking in, the market continued to rise, and the index reached 10.6%. Mr. C cannot unlock the feature to benefit from the additional growth, meaning he missed out on potential profits. - Limited profit potential: If the market continues to rise after the index has been locked, you will not benefit from the additional profits, which could reduce overall earnings potential.

- Low flexibility: The Index Lock feature is suitable for those with a long-term perspective and may not be ideal for investors who need quick liquidity or frequently change investment strategies.

How to maximize profits from the Index Lock feature

To fully leverage the benefits of the Index Lock feature, investors need to understand how and when to use this tool effectively.

- Choose the right time to lock in: Timing is critical when using the Index Lock feature. You need to closely monitor market movements and activate the feature when the index reaches its peak or when there are signs of an imminent market downturn.

- Combined with other investment strategies: The Index Lock feature works more effectively when combined with other insurance investment strategies, such as allocating resources into more stable insurance products to balance risks.

- Advice from financial experts: It is always recommended to seek advice from financial experts or insurance advisors to determine the best time to activate the Index Lock feature.

Thinksmart Insurance supports customers with profit lock

Which life insurance programs include the Index Lock feature?

The Index Lock feature is integrated into most of Allianz’s life insurance programs; however, only the Max Funded IUL Secrets maximizes the advantage of the Index Lock feature to generate the largest possible returns for retirement. Below are some of the characteristics that make the Index Lock feature fully optimized in Max Funded IUL:

- No negative floor: Max Funded IUL grows based on the S&P market index, and the higher the index, the larger the returns. Most importantly, even when the market declines into the negative, Max Funded IUL ensures a minimum floor of 0%—meaning you will never lose capital, thanks to the market downturn protection policy.

- Tax-free: All the accumulated funds from Max Funded IUL are tax-free upon withdrawal. This means that half of your retirement savings won’t be owed to taxes. Imagine how substantial this amount would be after 20 years of accumulation.

- Expert support team: Thinksmart Insurance continually monitors the market trends and will notify and support the Index Lock process if clients approve, without any additional fees.

- Allianz’s operating philosophy: Allianz, a long-established life insurance provider (since 1919), operates with a focus on investment growth. While other companies may integrate the Index Lock feature into their products, Allianz remains the most effective life insurance company in clearly defining and fully utilizing the Index Lock policy.

Conclusion

The Index Lock feature is a powerful tool to ensure returns and reduce risks in insurance investments. When used properly, the Index Lock feature can help you maximize your earnings despite market volatility. However, consider carefully the timing for activating the Index Lock.

Thinksmart Insurance has provided you with information about the Index Lock feature in various life insurance programs. If you have any questions or are interested in the Index Lock feature in the Max Funded IUL program, call the hotline at (678) 722 3447 or message us via Messenger and email Support@Thinksmartinsurance.com.

FAQs

- Can the Index Lock feature be applied to all types of life insurance?

No, the Index Lock feature is typically found only in Indexed Universal Life (ULIPs) or Indexed Annuity (FIAs) products, such as Max Funded IUL and other Allianz products. - Does the Index Lock feature protect my investment in case the market declines?

Yes, the Index Lock feature allows you to lock in the index value at its best point, securing profits even if the market drops. - Is my profit capped after activating the Index Lock?

Yes, once the Index Lock is activated, you will no longer benefit from subsequent market growth. - When is the best time to activate the Index Lock feature?

The best time is when the market reaches a peak and shows signs of significant volatility or decline. - Can I manually or automatically set an Index Lock target for different allocation options based on various goals?

Yes, if you have selected more than one allocation option, you can manually initiate a lock or set upper or lower targets for each indexed allocation. Different allocations may be locked at different times. - When will interest credits be applied to my policy?

Interest credits are applied at the end of the crediting period. Even if you manually initiate an Index Lock or the automatic Index Lock is triggered mid-period, the interest credit will not apply until the end of the crediting period. The crediting period ends on the next policy anniversary date. - The Index Lock has been activated (manually or automatically), and the index value has risen. Can I lock in a higher index value?

No. The Index Lock can only be activated once per allocation option during each crediting period. Once the index value is locked, it cannot be unlocked until the start of the next crediting period. - Does the locked index value become the starting value for the next crediting period?

No. If the Index Lock is activated, the starting index value for the next crediting period will be the index value at the end of the previous crediting period, not the locked index value. - If I request a manual Index Lock, when will the index value be locked?

If you request an Index Lock before 4:00 PM Eastern Time on a business day, the index will lock at that day’s closing value. If you request an Index Lock after 4:00 PM Eastern Time, the index will lock at the closing value of the next business day. The locked index value is the closing value on the business day the Index Lock is executed. Therefore, the actual locked index value could be higher or lower than the value at the time of the request. A business day is defined as any day the New York Stock Exchange (NYSE) is open for trading. Our business day ends when regular trading on the NYSE concludes. - How do I set an Auto Lock target?

Log into your account at www.allianzlife.com. In the “Allocations and Index Performance” section, click the Lock/Set Target button. After reading and agreeing to the notifications, click the allocation option for which you want to enter a target. Set your target based on the indexed interest rate and the applicable participation rate. - How do I cancel a target?

Similar to setting a target, you can cancel a target anytime by logging into your account online. Once logged in, navigate to the “Allocations and Index Performance” section and cancel the target you wish to remove. - Can I modify set targets?

Yes. You can modify targets at any time, as long as the Auto Lock has not been triggered for that allocation option within the current crediting period. - Do I need to set a new target for each crediting period?

You must set a new target for each crediting period unless the automatic renewal feature is active. The auto-renew feature is only available for one-year allocation option targets. If you do not choose auto-renew or want to set new targets, you can do so as soon as the new crediting period begins. - Do I need to set lower targets for each crediting period?

Yes. Lower targets can only be set if the Index Lock hasn’t occurred. They must be set below the current indexed interest rate and must be greater than zero. - If I set upper and/or lower targets and the target is reached, am I guaranteed to receive that indexed interest rate?

No. The Index Lock will be triggered at the end of the business day if the target is reached. For this reason, the indexed interest rate you receive may be higher than your upper target or lower than your lower target. - What happens if my target is not reached by the end of my crediting period?

If a target is not met during your crediting period, you will receive interest credits based on the index value at the end of your crediting period. - Can I manually activate the Index Lock if I have already set a target?

Yes, you can manually activate the Index Lock at any time, as long as the Index Lock has not already been triggered.

Thinksmart Insurance

Thinksmart Insurance