Kaizen Insurance is a relatively new type of life insurance compared to traditional Whole Life. In recent years, Kaizen has garnered much attention due to its highly profitable retirement accumulation formula. This article will delve into what Kaizen insurance is, how it works, its pros and cons, and compare Kaizen with IUL Secrets, Term Life, and Whole Life.

What is Kaizen Insurance?

Kaizen Insurance is an advanced IUL type of life insurance that combines the benefits of traditional life insurance (living benefits and death benefits) with financial techniques (leverage) to provide a comprehensive insurance solution with multiple times the earning potential.

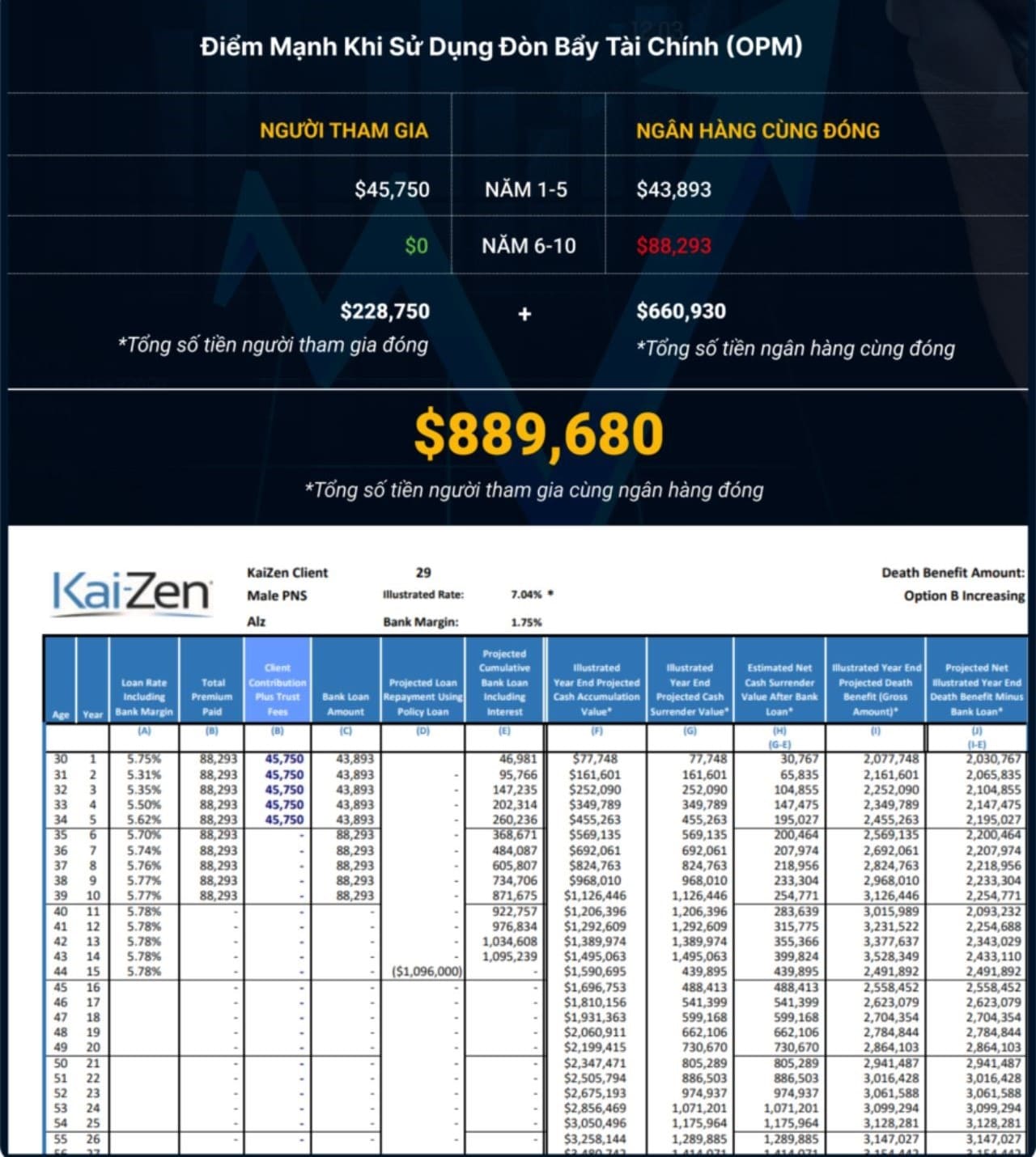

When participating in Kaizen insurance, a third party (usually banks) will loan the buyer additional money to pay the policy at a 3:1 ratio (i.e., the bank pays 3 parts, the buyer only pays 1 part). Thus, participants in Kaizen insurance will receive protection benefits and a retirement accumulation amount four times higher than other types of life insurance such as IUL Secrets, Term Life, and Whole Life.

Kaizen Insurance 3:1 Formula

To achieve this high earning potential, Kaizen Insurance companies use financial leverage through bank loans. However, rest assured that the buyer only needs to pay the insurance for the first 5 years, and the bank will cover the rest (3:1 ratio) for the next 5-10 years. The unique feature of Kaizen is the 100% guarantee that buyers will not be in debt from the bank loans; their concern is only to complete the payments within the first 5 years.

Example Illustration of Kaizen Insurance Payments According to the 3:1 Formula

Kaizen Insurance is particularly suitable for high-income individuals such as executives, doctors, and other professionals who seek enhanced retirement plans and financial protection without depleting current assets.

How Does the Kaizen Policy Work?

Kaizen Insurance policy operates through a carefully structured process involving multiple parties, including the participant, life insurance company, and third-party lender. Here are the detailed steps of how the Kaizen policy works:

- Initial Premium Payment: The participant must contribute the initial Kaizen insurance premium, usually the first 5 years of the policy. This initial money represents the participant’s commitment and helps establish the policy’s cash value.

- Third-Party Financing: After the initial contribution, a third-party lender will fund the remaining premiums. The loan is secured by the policy’s cash value, meaning the participant does not need to undergo a financial appraisal or prove personal financial/assets capacity for the loan. Here, the life insurance policy acts as the sole collateral.

- Policy Growth and Cash Value Accumulation: The cash value of the Kaizen policy grows over time based on the performance of selected market indices. The policy is designed with a “floor” and a “ceiling,” meaning it can benefit from market growth and not lose even when the market declines.

- Loan Repayment: The loan from the third-party lender is typically repaid by the accumulated cash value. This repayment process occurs around the 15th year of the policy, after which Kaizen participants have full access to the cash value.

- Ongoing Policy Management: Throughout the policy’s life, participants receive annual reports and reviews from administrators, providing updates on the policy’s performance, cash value growth, and any remaining loan balance.

By leveraging third-party financing, the Kaizen insurance policy allows participants to own a larger death benefit and greater living benefits than their self-financing capabilities. This innovative approach enhances financial protection and provides a substantial supplementary retirement income.

Pros and Cons of Kaizen Insurance

Like any financial product, Kaizen Insurance has its advantages and disadvantages. Buyers need to understand these to decide whether Kaizen insurance suits their financial goals and needs.

Pros

- Extended Insurance: Kaizen Insurance allows buyers to own a life insurance policy with significantly larger death and living benefits than their financial capabilities.

- Leverage and Financing: By leveraging third-party financing, Kaizen Insurance enables participants to maximize life insurance benefits without significantly depleting current financial resources. The use of leverage helps to purchase a higher cash value policy, leading to greater cash value accumulation and potential retirement income.

- Tax Benefits: The cash value in a Kaizen insurance policy grows tax-free. Additionally, policy loans are typically tax-free, providing higher retirement income.

- Market Protection: Kaizen Insurance protects against market volatility. With a “floor” to prevent losses during market downturns and a “ceiling” to participate in market growth, the policy offers a balanced approach to growth and security.

- Flexibility and Access: After the loan is repaid, Kaizen participants have full access to the accumulated cash value, which can be used for various financial needs, including retirement income, education costs, or emergency funds. This flexibility makes Kaizen Insurance a versatile tool for long-term financial planning.

- No Personal Liability: The loan used to pay for the insurance is secured by the life insurance policy, so participants are not personally liable for the debt.

Cons

- Complexity: The Kaizen Insurance “formula” involves multiple parties and financial mechanisms, making it more complex than traditional life insurance products.

- Eligibility Requirements: Kaizen Insurance is designed for high-income individuals who meet specific criteria, such as a minimum annual income (typically around $100,000/year or total assets over $1,000,000) and good health.

- Initial Commitment: Participants must contribute the initial premium, usually covering the first 5 years of the policy. This initial investment can be large and not feasible for everyone.

- Loan Repayment: Kaizen insurance participants need to ensure they have enough money to cover the first 5 years of payments.

- Limited Access to Funds: Until the loan is fully repaid, participants have limited access to the cash value and policy benefits.

Comparison of Kaizen Insurance with IUL, Term Life & Whole Life

Kaizen Insurance is a unique life insurance strategy offering distinct benefits compared to other popular life insurance products. Below is a comparison between Kaizen Insurance, IUL Secrets, Term Life, and Whole Life:

|

Criteria |

Kaizen Insurance | IUL Secrets | Term Life Insurance |

Whole Life Insurance |

| Death Benefit | Flexible with cash value growth | Flexible with cash value growth | Fixed within the policy term | Fixed for life |

| Living Benefits | 15 different diseases and disabilities | 16 different diseases and disabilities | Usually none or less flexible than Kaizen and IUL Secrets | Usually none |

| Compensation Level | High growth potential through leverage | Depends on market performance with growth limits | Fixed compensation if death occurs within the term | Stable guaranteed growth and fixed death benefit |

| Time | Requires contributions for 5 years; long-term insurance | Permanent insurance with flexible premiums | Fixed term (e.g., 10, 20, 30 years) | Lifetime insurance with fixed premiums |

| Participation Fees and Costs | High initial contribution; leverage reduces costs | High costs due to market-linked growth | Lower costs than permanent insurance | Higher costs but fixed for life |

| Profitability | High growth potential through leverage | High growth potential but with market risk | No cash value or growth | Guaranteed cash value growth and dividends |

| Conditions | Requires good health and high income | Suitable for high-risk takers | Ideal for those needing temporary protection | Suitable for those seeking long-term stability |

| Suitable For | High-income individuals aged 18-65 with good health | Those wanting to combine insurance with investment | Those needing temporary protection (e.g., young families) | Those seeking lifetime insurance and estate planning |

| Other Factors | Leverage does not require personal guarantees or interest repayment | Requires active management; high complexity | Simple, easy to understand, and low-cost | Stability, financial predictability, and fixed premiums |

Comparison table of Kaizen Insurance with IUL Secrets, Term Life & Whole Life

Conclusion on Kaizen Insurance

Kaizen Insurance is a life insurance strategy combining the benefits of IUL with third-party financing to expand cash value growth and generate substantial retirement income.

Despite its complex operation and challenging participation conditions, the benefits of Kaizen Insurance make it an attractive option for high-income individuals seeking a life insurance product with comprehensive living and death benefits, a highly profitable financial solution, and superior tax-efficient retirement accumulation.

For more information about Kaizen Insurance, please contact Thinksmart Insurance via email at Support@Thinksmartinsurance.com, message through the Messenger app, or call the hotline at (678) 825 3737.

Thinksmart Insurance

Thinksmart Insurance